ESG - Index

What is the significance of ESG?

ESG stands for Environmental, Social & Governance. It is an assessment framework that evaluates companies on three pillars: environmental impact, social responsibility, and good governance. ESG helps organizations gain insight into their sustainability performance and non-financial risks.

The significance of ESG therefore extends beyond sustainability alone. It encompasses climate impact, working conditions, diversity, ethical business practices, transparency, and risk management, among other factors. Investors, regulators, and customers are increasingly using ESG criteria to determine how future-proof and responsible an organization operates.

For companies, ESG means that they must not only pursue financial returns, but also take into account their impact on people, the environment, and governance structures.

Once upon a time, there was a company committed to ESG, where a group of employees decided to organise an eco-friendly office competition. They challenged each other to use as little paper as possible for one month. People started coming up with the most creative solutions as part of this hilarious contest, including folded envelopes and even origami artworks made from recycled memos. Ultimately, the employees ended up saving trees, in addition to boosting workplace togetherness as they addressed this ESG challenge. So as you can see, small changes can make a big impact.

What is ESG?

ESG is an acronym that stands for Environmental, Social, and Governance. It is a framework used to assess the sustainability and social impact of businesses and organisations. Sounds familiar? Is ESG the same as Corporate Social Responsibility (CSR)? They are very similar. CSR and ESG both pursue and promote climate-friendly and social-ethical business practices. However, ESG is the more widely known international standard. Several (European) standards have been defined, facilitating reporting for (international) companies.

Interesting read: ESG is the new corporate social responsibility

Where does the term ESG come from?

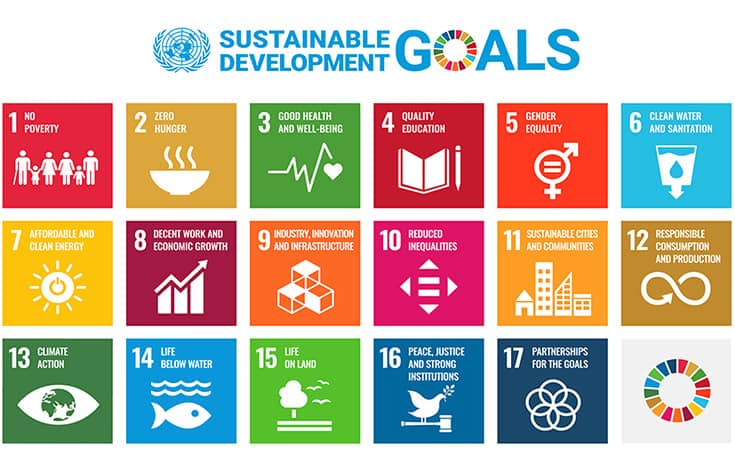

ESG has its roots in the 17 Sustainable Development Goals (SDGs) that were identified by the United Nations (UN) to end poverty, pursue economic growth, and take climate action.

ESG factors can be linked to the SDGs at company level. The 17 SDGs have been transposed into 10 foundational ESG principles, that help businesses develop an ESG strategy that drives their business practices.

- Businesses should support and respect the protection of international human rights.

- Businesses must make sure they are not complicit in human rights abuses.

- Businesses should uphold the freedom of association and the effective recognition of the right to collective bargaining.

- The elimination of all forms of forced and compulsory labour.

- The effective abolition of child labour.

- The elimination of discrimination in respect of employment and occupation.

- Businesses should support a precautionary approach to environmental challenges.

- Businesses should undertake initiatives to promote greater environmental responsibility.

- Businesses should encourage the development and diffusion of environmentally friendly technologies.

- Businesses should work against corruption in all its forms, including extortion and bribery.

What makes a good ESG policy?

In 2023, simply claiming to embrace the SDGs is no longer sufficient. An effective ESG policy requires a more in-depth approach, in which you actively look at ways of creating positive impact with your daily business practices. Actions speak louder than words and concrete action is essential for contributing to sustainability, social responsibility, and good governance.

Setting measurable targets is a crucial part of a good ESG policy. These metrics allow you to measure and evaluate the progress and effectiveness of your sustainability efforts. The problem, however, is not the metrics or the targets. Reporting and way in which results are measured could also do with more standardisation.

ESG reporting

ESG reports contain qualitative and quantitative metrics about your company’s performance in terms of environment, society, and governance. In it, you shed light on your company's ESG activities, increase transparency for investors, and inspire other organisations to follow your example. In addition, you show how you achieve your goals and that your ESG projects are genuine; i.e., that you are not guilty of ‘greenwashing’. This term is used for businesses that mislead their audience by pretending to be more environmentally-friendly or sustainable than they really are.

Preparing and structuring an ESG report is a challenging undertaking for most companies because ESG metrics vary depending on the industry, company size, and complexity. Legislation and reporting standards also have an important role in this.

Interesting read: The challenges of an ESG-strategy

How do I write a good ESG report?

- Environmental

Refers to the activities a business undertakes to be environmentally-friendly, such as reducing emissions or promoting energy efficiency. This looks at:

- How a business commits to fighting climate change.

- Which measures a business takes to reduce CO2 emissions.

- How a business contributes to preserving biodiversity, improving air and water quality, preventing deforestation, and managing waste responsibly.

- How a business uses natural resources sustainably and ensures a responsible supply chain.

- Which efforts a business makes to reduce its own emissions. - Social (sociaal)

Refers to a company's relationships with its employees, customers, communities, and other stakeholders. This includes:

- How a business promotes the well-being of its employees and creates a safe working environment.

- Which efforts a business makes to promote gender inclusion and ensure LGBTQ+ inclusion in the workplace

- How a business promotes employee engagement.

- Measures taken to ensure data protection and privacy.

- A company's social commitment.

- Compliance with human rights and labour standards. - Governance Refers to the way a business is governed and managed. This includes how transparent a business is in its financial reporting, but also pertains to (un)ethical business practices, the independence of its directors, and the presence of internal controls. It examines:

- A company's internal controls.

- How policies, principles and procedures on leadership, board structure, compensation of directors, audit committee, shareholder rights, prevention of bribery, lobbying practices, political donations, and protection of whistleblowers are established.

What is an ESG score?

An ESG score is very similar to a credit rating, albeit for sustainability. It provides a measure of how well a business scores in terms of environmental issues, social responsibility, and good governance. It also reveals the extent to which the company adheres to its sustainability commitments, how well it performs in these areas, and the risks it faces.

ESG scores are a relatively new development and can therefore be exposed to liabilities. Many companies that offer ESG scores rely on information provided by businesses themselves. As a result, there may be a discrepancy between the score and the company’s actual sustainability performance.

A balanced approach is therefore crucial to improve ESG scores and make them more accurate. Good ESG scoring involves a mix of sources of information, including data from businesses themselves, as well as the use of technologies such as Natural Language Processing (NLP) and machine learning, such as AI.

How do I get an ESG score?

ESG laws and regulations

In recent years, numerous laws and regulations have been laid down regarding ESG, mainly at European level. These laws are mainly aimed at large companies, but as their entire supply chain must also comply with these frameworks, this often has a significant impact on smaller companies. As time goes on, SMEs will increasingly play a part in ESG regulatory and legislative compliance.

Wondering which rules apply to your business?

Below we list the most important ESG laws and regulations.

Sustainable Finance Disclosure Regulation (SFDR)

The SFDR took effect in March 2021. This important regulation is applicable to financial market participants, such as pension funds, investment managers, and similar institutions, imposing an obligation on them to disclose sustainability information about their products. The scope covers the end result of their investment processes, as well as justification for the sustainability risks taken.The SFDR is thorough and detailed, requiring a considerable amount of disclosure. It is worth noting that this law applies to all financial market participants, regardless of whether they are actively engaged in sustainability or not. Even stricter rules apply if an institution offers sustainable products.

Taxonomy Regulation

Since January 2022, financial market participants are required by law to provide a common framework of terms to communicate about sustainable and responsible investments (SRIs) in an unambiguous way. This new regulation aims to promote clarity and transparency within the industry and contribute to a better understanding of SRIs.Corporate Sustainability Reporting Directive (CSRD)

The CSRD is an important step for companies operating within the European Union (EU), enabling them to identify ESG risks and provide sustainability information to their stakeholders. This directive is an extension of the existing Non-Financial Reporting Directive (NFRD), which has applied to the largest companies in the EU since 2014. The CSRD applies to companies that meet at least two of the following three criteria:- The company has more than 250 employees.

- The company has an annual net turnover of more than 40 million euros.

- Balance sheet total assets are greater than 20 million euros.

The new CSRD will take effect from January 2024 and will cover financial year 2023. This means that companies should start preparing their ESG documentation as early as 2023 to meet the compliance requirements by 2024. The CSRD is expected to also become applicable to smaller companies within the EU in the coming years. Currently, small and medium enterprises (SMEs) are exempt from CSRD reporting obligations until financial year 2026, but before this they will already have to contend with requirements from their supply chain partners that do fall under the CSRD obligation.

The Corporate Sustainability Due Diligence Directive (CSDD)

On 1 June 2023, the EU adopted the CSDD, aimed at encouraging companies to integrate human rights and environmental protection into their business operations. The new rules apply to:Business records | worldwide net sales* | Employees |

|---|---|---|

EU-based companies | > 40 million euros | > 250 employees |

EU-based parent companies | > 150 million euros | > 500 employees |

Non-EU-based companies | > 150 million euros, of which at least €40 million was generated in the EU | Not applicable |

Non-EU-based parent companies | > 150 million euros, of which at least €40 million was generated in the EU | > 500 employees |

*When determining the threshold for the total net turnover generated by a non-EU-based company within the European Union, it is worth noting that this does not only refer to the direct revenues of the company itself. This also includes revenues derived from collaborations with other companies in the EU, e.g., in cases where the non-EU-based company has concluded agreements for the use of its products or brand in exchange for payment.

This directive requires companies subject to the CSDD to make their due diligence strategy public. In it, they must indicate how they deal with such issues as child labour, slave trade, emissions, corruption, and so on. This will have an impact on their own supply chain, but also on any suppliers and contractors, both inside and outside the EU.

The legislation may cause companies subject to the CSDD to request documentation from smaller businesses to demonstrate compliance with their due diligence obligations because CSDD-regulated companies have a duty to ensure that their partners and suppliers also comply with sustainability standards. In all likelihood, the CSDD will only take effect around 2025-2026 at the earliest.

ESG reporting standards

Preparing an ESG report is further complicated by the multiple reporting standards you can choose from. The best-known ESG reporting standards are:

The Global Reporting Initiative (GRI)

The GRI is an international independent standards organisation that helps companies take responsibility for their impacts. The GRI Standard promotes uniform communication on a company’s impacts and consists of Universal, Sector and Topic Standards. These provide a structured approach to produce a comprehensive ESG report or to mention specific topics on websites or in partial reports.The Sustainability Accounting Standards Board (SASB)

The SASB has developed an ESG framework to facilitate ESG reporting. It distinguishes between different industries and differentiates based on the chosen industry, given that the focus may vary. Instead of a template, the framework provides a comprehensive list of topics for writing a good ESG report. Given that it was developed in the USA, it takes into account American standards.The Task Force on Climate-related Financial Disclosures (TCFD)

The TCFD, which was created in 2015 by the Financial Stability Board, seeks to facilitate uniform ESG reporting. Originating from the UN, it targets banks, insurers and investors. The aim is to promote increased transparency in the financial sector on sustainability for a more stable and sustainable economy.The Carbon Disclosure Project (CDP)

Although the CDP originally focused on measuring and reporting CO2 emissions, it has since expanded to include other environment-related aspects. The CDP collects data from thousands of companies on their environmental performance and disclosure, making it publicly available to investors and the public.Integrated Reporting (IR)

Integrated Reporting encourages the integration of financial and non-financial information in one report, with an emphasis on long-term value creation. This enables companies to give a comprehensive overview of their performance and impact, and how they generate value for all stakeholders.The International Sustainability Standards Board (ISSB)

Recently, the ISSB launched two new standards, namely IFRS S1 and IFRS S2. These are designed to be seamlessly integrated into corporate financial reporting. IFRS S1 focuses on general sustainability reporting and uses TCFD principles for non-climate related topics. IFRS S2, meanwhile, covers climate-related issues, such as emissions and risks, and uses TCFD approaches. These new standards allow business to report on sustainability and financial information in an integrated and standardised way.Choosing the right reporting standard is crucial and that is what makes ESG reporting so challenging. You need to carefully consider which standard is most relevant to your specific industry, business model, and stakeholders. One standard may be more suited to the nature of your business activities, while another may place more emphasis on your company’s environmental or social impacts.

What benefits does ESG reporting have for my business?

Besides regulatory compliance, sustainability reporting has many other benefits for business owners!

- Improved sustainability performance ESG reports help companies to map their impact on the environment, society, and their governance practices. This promotes awareness and accountability, leading to improved sustainability performance and the ability to adapt strategies for long-term positive impact.

- Better risk management By analysing non-financial factors, businesses can identify potential risks that would otherwise be overlooked. ESG reporting provides insight into such issues as climate change, reputational risks, supply chain vulnerabilities and more, allowing companies to act proactively to mitigate risks.

- Greater appeal for investors More and more young investors are focusing on sustainability and ESG criteria in their decision-making. ESG reporting can make the company more attractive for investors looking for a long-term return and positive social impact.

- Stronger relationships with stakeholders ESG reporting promotes transparency and trust among customers, employees, suppliers, and communities. It shows commitment to social issues and enhances the company's credibility.

- Innovation and efficiency Analysing ESG performance can lead to innovative solutions for more sustainable operations, generating cost savings and creating competitive advantages in a rapidly changing business environment.

- Positive reputation Companies that actively report on their ESG efforts as part of their commitment to sustainability build a positive reputation with customers, employees, and other stakeholders, which, in turn, helps to attract and retain talent and customers.